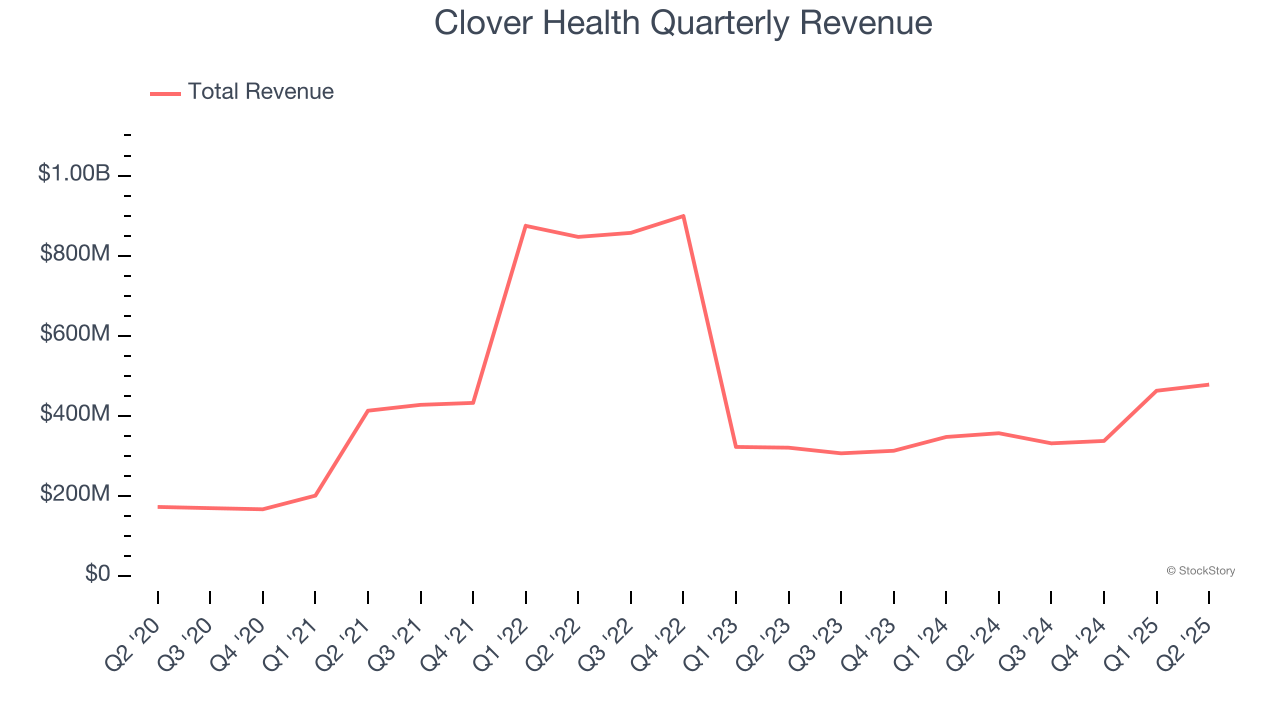

Health insurance company Clover Health (NASDAQ:CLOV) reported revenue ahead of Wall Street’s expectations in Q2 CY2025, with sales up 34.1% year on year to $477.6 million. Its GAAP loss of $0.02 per share was in line with analysts’ consensus estimates.

Is now the time to buy Clover Health? Find out by accessing our full research report, it’s free.

Clover Health (CLOV) Q2 CY2025 Highlights:

- Revenue: $477.6 million vs analyst estimates of $469.5 million (34.1% year-on-year growth, 1.7% beat)

- EPS (GAAP): -$0.02 vs analyst estimates of -$0.03 (in line)

- Adjusted EBITDA: $17.14 million vs analyst estimates of $16.93 million (3.6% margin, 1.2% beat)

- EBITDA guidance for the full year is $60 million at the midpoint, above analyst estimates of $56.2 million

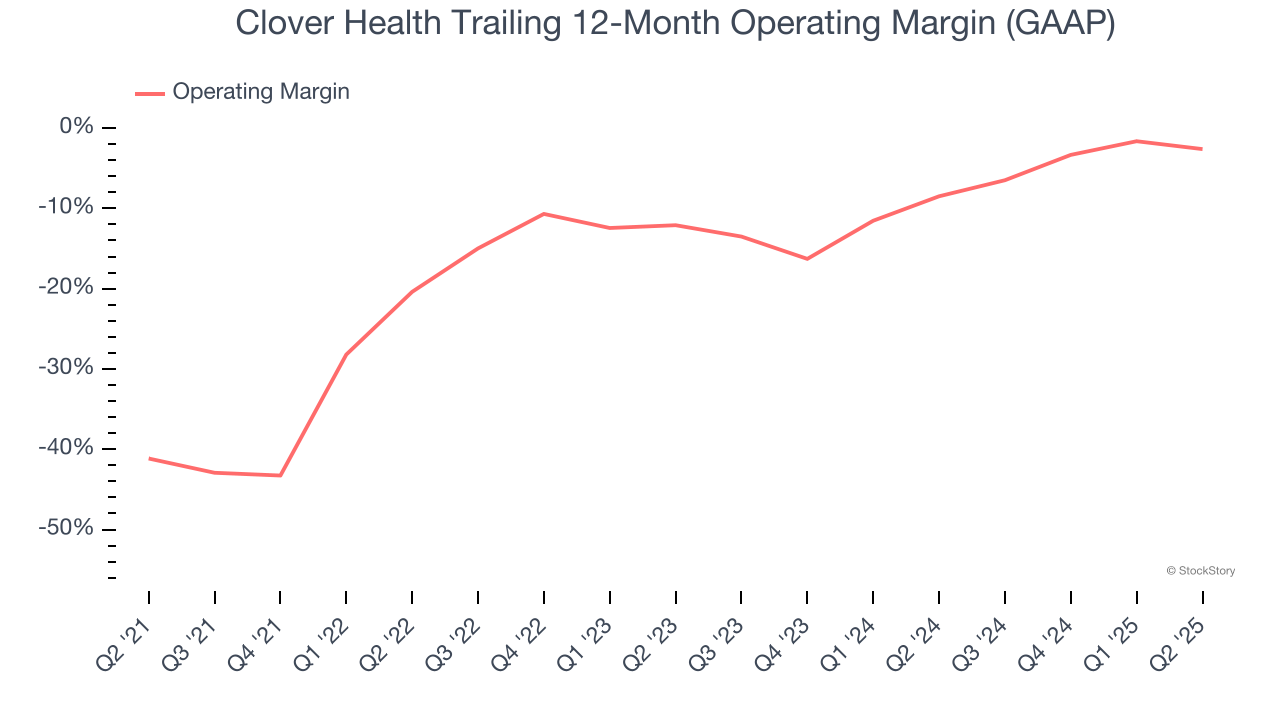

- Operating Margin: -2.2%, down from 2% in the same quarter last year

- Free Cash Flow Margin: 1%, down from 12.5% in the same quarter last year

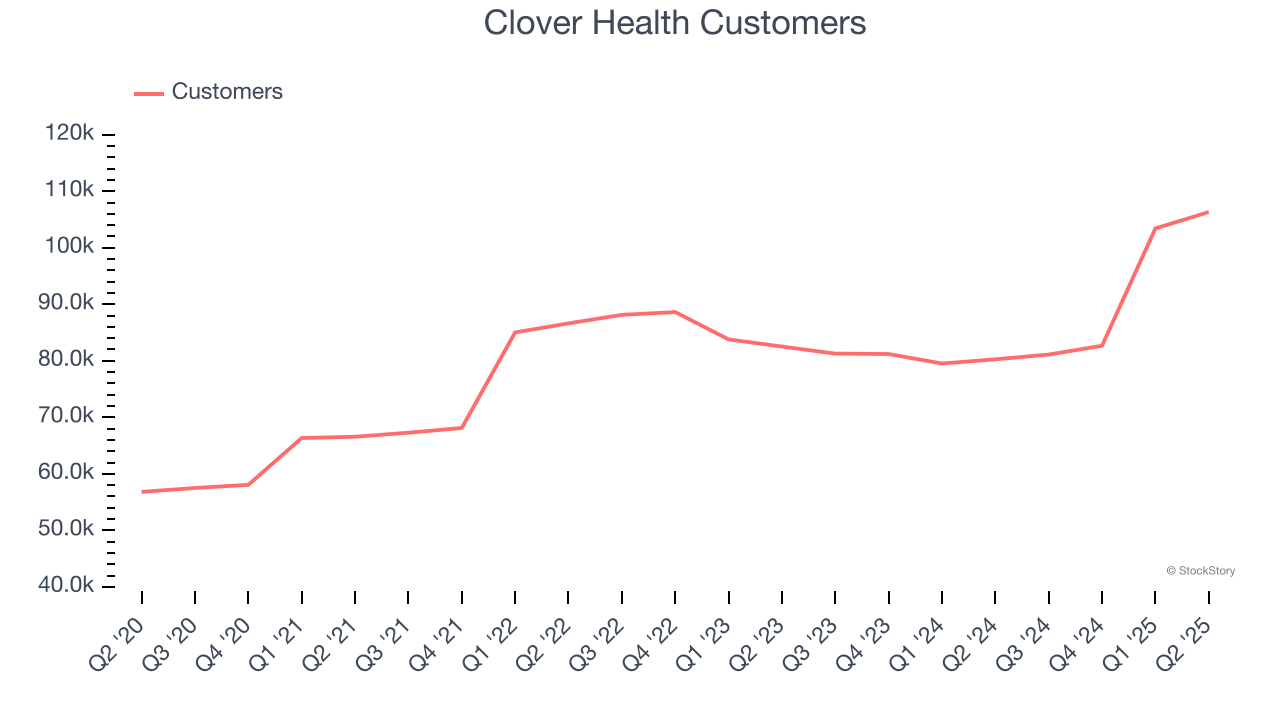

- Customers: 106,323, up from 103,418 in the previous quarter

- Market Capitalization: $1.47 billion

"Our performance further demonstrates how our technology-first model drives better care management, above-market growth, and sustained profitability," said Clover Health CEO Andrew Toy.

Company Overview

Founded in 2014 to improve healthcare for America's seniors through technology, Clover Health (NASDAQ:CLOV) provides Medicare Advantage plans for seniors with a focus on affordable care and uses its proprietary Clover Assistant software to help physicians manage patient care.

Revenue Growth

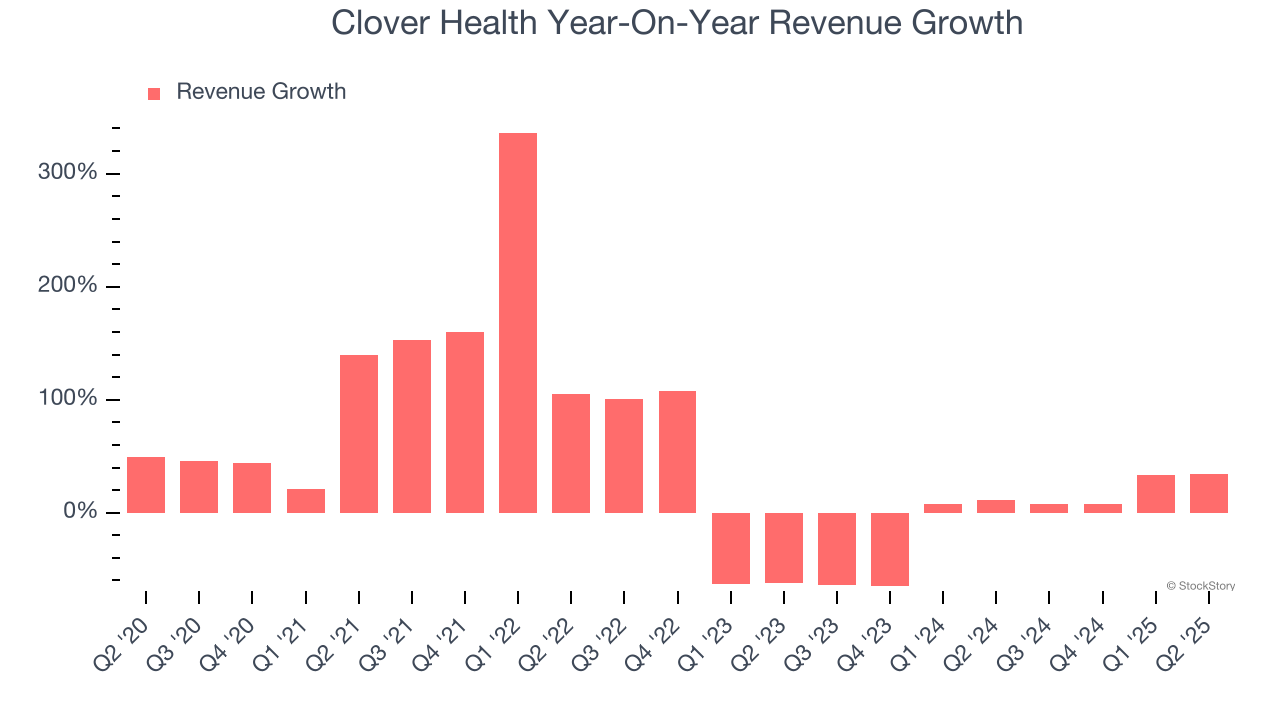

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Clover Health’s sales grew at an excellent 23.1% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Clover Health’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 18.1% over the last two years.

Clover Health also reports its number of customers, which reached 106,323 in the latest quarter. Over the last two years, Clover Health’s customer base averaged 5% year-on-year growth. Because this number is better than its revenue growth, we can see the average customer spent less money each year on the company’s products and services.

This quarter, Clover Health reported wonderful year-on-year revenue growth of 34.1%, and its $477.6 million of revenue exceeded Wall Street’s estimates by 1.7%.

Looking ahead, sell-side analysts expect revenue to grow 31.2% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and suggests its newer products and services will spur better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Clover Health’s high expenses have contributed to an average operating margin of negative 15.4% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Clover Health’s operating margin rose by 38.5 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 9.5 percentage points on a two-year basis.

Clover Health’s operating margin was negative 2.2% this quarter.

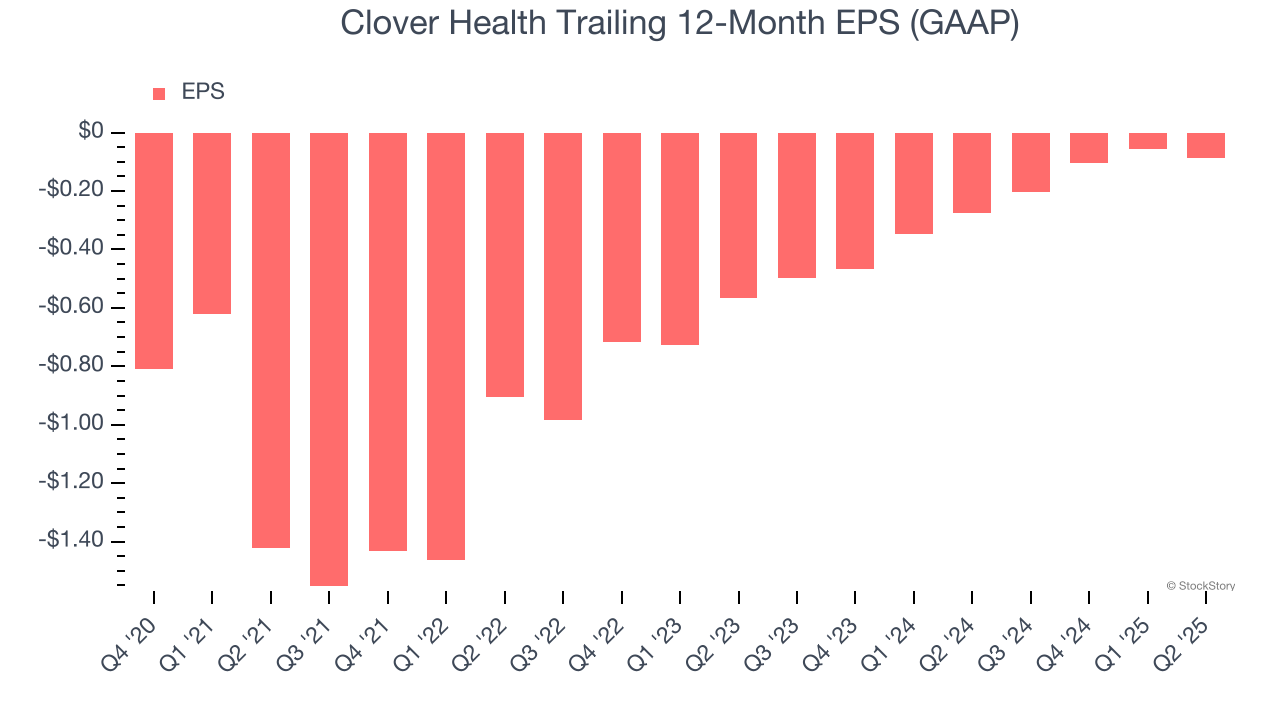

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Clover Health’s full-year earnings are still negative, it reduced its losses and improved its EPS by 40.3% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q2, Clover Health reported EPS at negative $0.02, down from $0.01 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Clover Health’s full-year EPS of negative $0.09 will reach break even.

Key Takeaways from Clover Health’s Q2 Results

We enjoyed seeing Clover Health beat analysts’ revenue and EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. Zooming out, we think this was a solid print. Investors were likely hoping for more, and shares traded down 7.9% to $2.61 immediately following the results.

Is Clover Health an attractive investment opportunity right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.