Cloud computing and online retail behemoth Amazon (NASDAQ:AMZN) met Wall Street’s revenue expectations in Q1 CY2025, with sales up 8.6% year on year to $155.7 billion. The company expects next quarter’s revenue to be around $161.5 billion, close to analysts’ estimates. Its GAAP profit of $1.59 per share was 17.2% above analysts’ consensus estimates.

Is now the time to buy Amazon? Find out by accessing our full research report, it’s free.

Amazon (AMZN) Q1 CY2025 Highlights:

- Revenue: $155.7 billion vs analyst estimates of $155 billion (in line)

- Operating Profit (GAAP): $18.41 billion vs analyst estimates of $17.52 billion (5% beat)

- EPS (GAAP): $1.59 vs analyst estimates of $1.36 (17.2% beat)

- Revenue Guidance for Q2 CY2025 is $161.5 billion at the midpoint, roughly in line with what analysts were expecting

- North America Revenue: $92.89 billion vs analyst estimates of $92.53 billion (small beat)

- AWS Revenue: $29.27 billion vs analyst estimates of $29.38 billion (small miss)

- North America Operating Profit: $5.84 billion vs analyst estimates of $6.01 billion (2.9% miss)

- AWS Operating Profit: $11.55 billion vs analyst estimates of $10.43 billion (10.7% beat)

- Operating Margin: 11.8%, up from 10.7% in the same quarter last year

- Free Cash Flow Margin: -5.1%, down from 3.5% in the same quarter last year

- Market Capitalization: $1.96 trillion

“We’re pleased with the start to 2025, especially our pace of innovation and progress in continuing to improve customer experiences,” said Andy Jassy, President and CEO, Amazon.

Revenue Growth

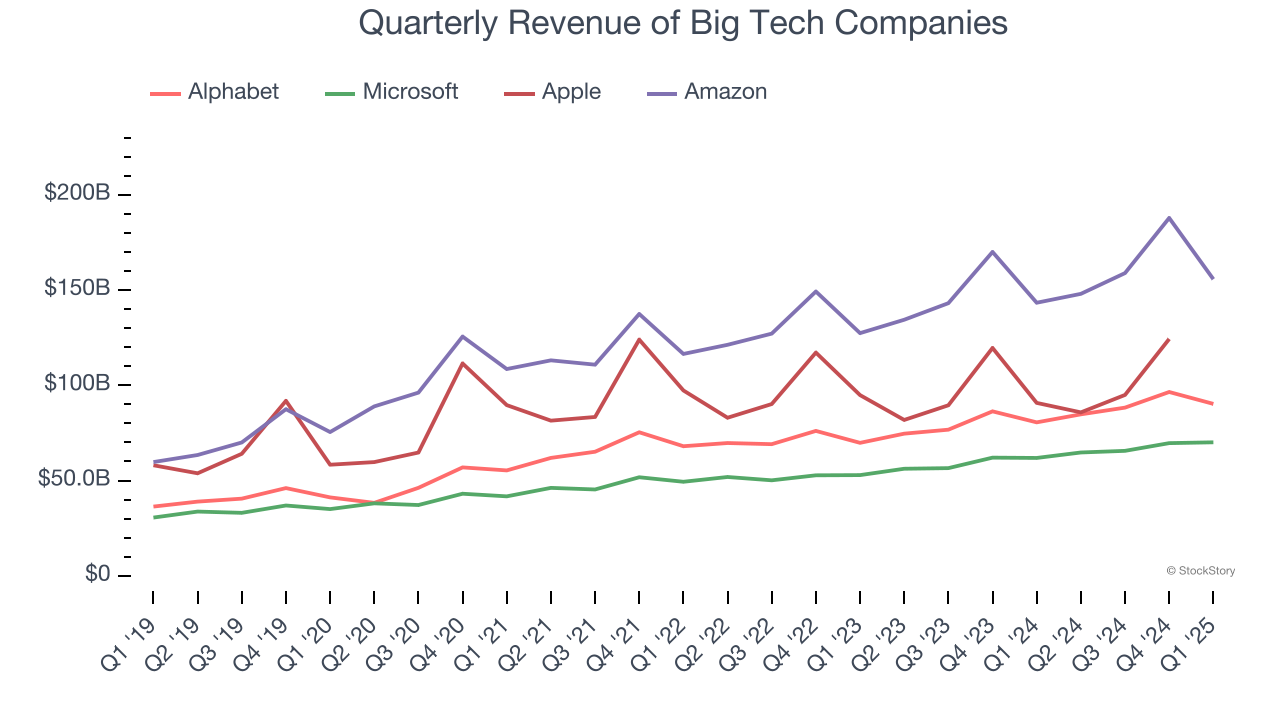

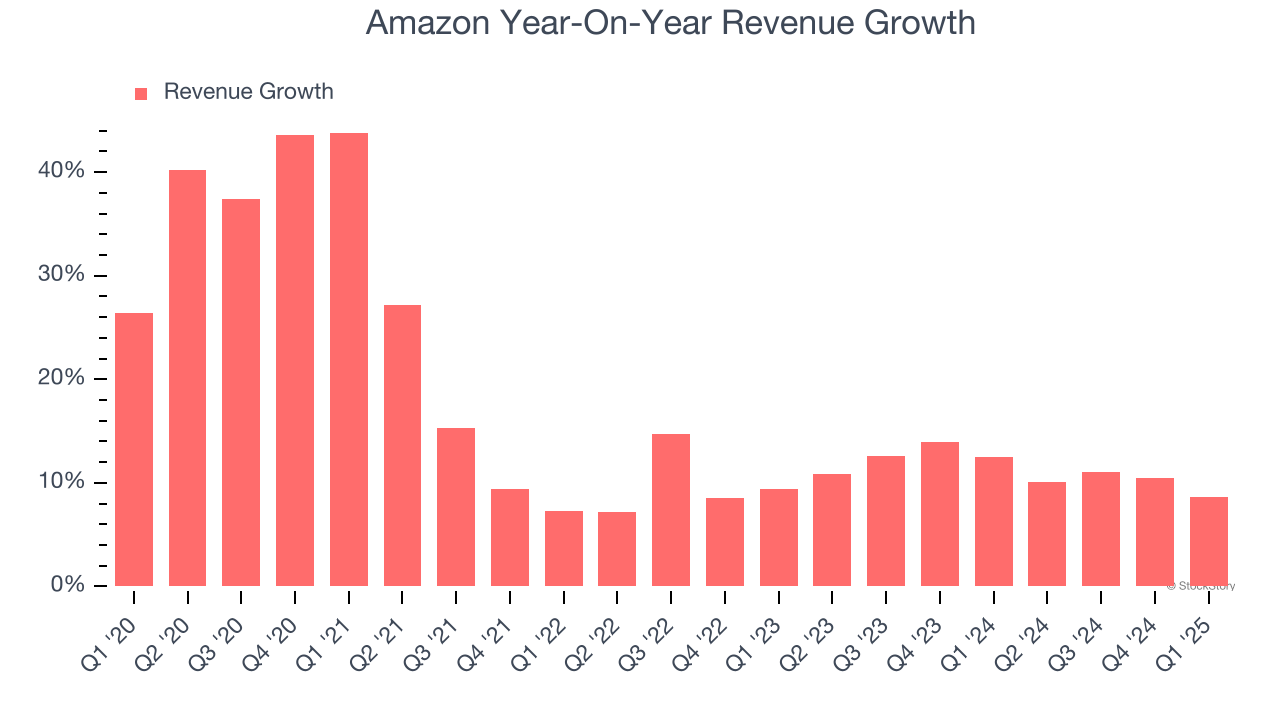

Amazon shows that fast growth and massive scale can coexist despite the conventional wisdom about the law of large numbers. The company’s revenue base of $296.3 billion five years ago has more than doubled to $650.3 billion in the last year, translating into an incredible 17% annualized growth rate.

Amazon’s growth over the same period was also higher than its big tech peers, Alphabet (16.6%), Microsoft (14.3%), and Apple (8.1%). This is an important consideration because investors often use the comparisons as a starting point for their valuations.

Long-term growth reigns supreme in fundamentals, but for big tech companies, a half-decade historical view may miss emerging trends in AI. Amazon’s annualized revenue growth of 11.3% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Amazon grew its revenue by 8.6% year on year, and its $155.7 billion of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 9.1% year-on-year increase in sales next quarter. Looking further ahead, sell-side analysts expect revenue to grow 9% over the next 12 months, a slight deceleration versus the last two years. This projection is still healthy and illustrates the market sees some success for its newer products.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Profitability: The Key Debate

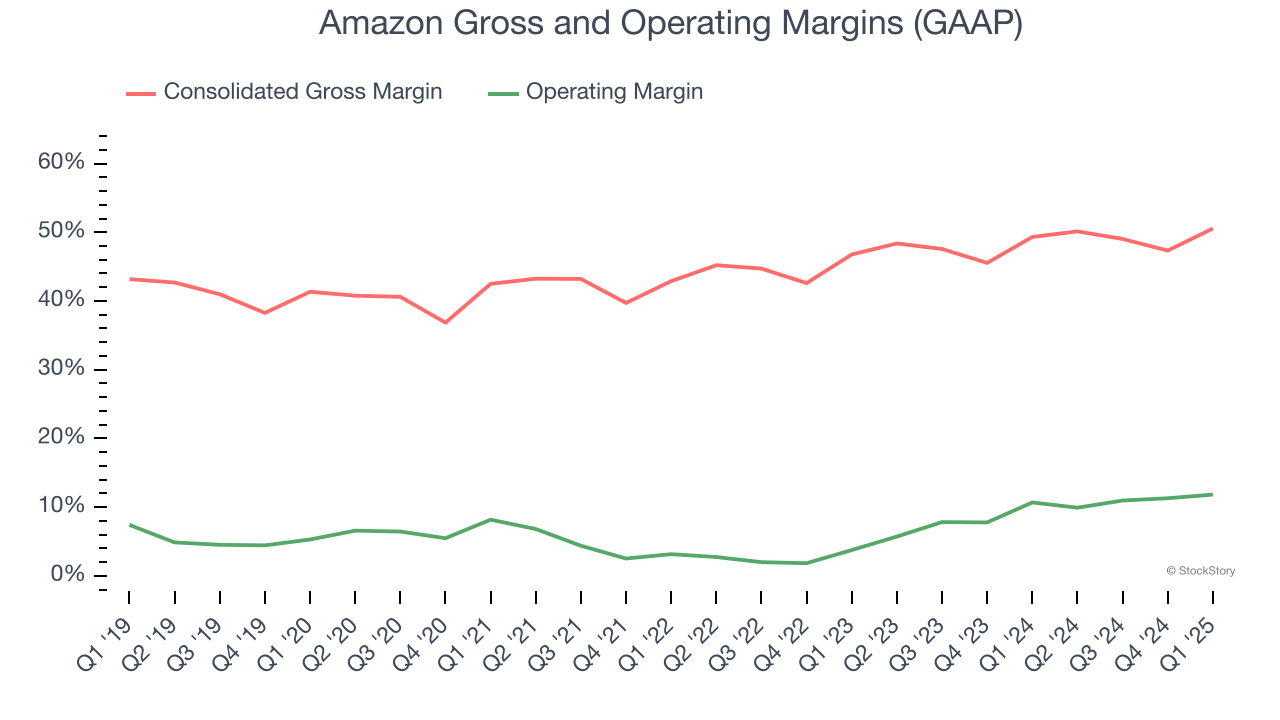

Many investors understand that Amazon’s e-commerce business caps its gross margin, which averaged 45.2% over the last five years. The company lags behind its pure-play tech peers because it sells many commoditized goods online where it must acquire and hold physical inventory.

What the market debates, however, is where Amazon’s long-term operating profitability could ultimately settle. Sure, its five-year margin of 6.8% was weak, but it rose by 4.4 percentage points thanks to leverage on the fixed costs in its consumer-facing businesses and the highly profitable AWS segment becoming a larger portion of its revenue. Our question is if Amazon’s momentum can continue and result in a mid-to-high teen percentage margin somewhere down the line.

The company’s North America segment holds the keys to this answer. Throughout the years, Amazon has made huge investments to not only attract hoards of customers into its ecosystem but also retain them. Some areas of focus in this effort included its unmatched delivery network and video streaming content.

Bulls will argue that Amazon can afford to ease up and begin riding its investments of the last two-plus decades. Wall Street seems to disagree somewhat and is projecting its trailing 12-month operating margin of 11% to stagnate in the coming year.

Key Takeaways from Amazon’s Q1 Results

We enjoyed seeing Amazon beat analysts’ EPS and operating income expectations this quarter, but the results were a bit messier when looking under the hood - the North America segment's operating income missed, which is the key debate for the stock. On top of that, its operating income guidance for next quarter missed significantly. Zooming out, we think this was a mixed quarter with a weak outlook. The stock traded down 3.5% to $183.16 immediately after reporting.

Is Amazon an attractive investment opportunity at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.