In a market where protecting capital matters as much as chasing gains, dividends feel like a steady paycheck. They offer investors a tangible return, even when price action turns volatile. And when a company keeps raising that payout, it usually means management feels confident about the company’s earnings visibility and balance sheet strength – basically, things are running smoothly behind the scenes. It reflects disciplined cash flow management, healthy liquidity, and suggests there’s enough left after running the business to reward shareholders. Not every company can pull that off consistently.

That brings us to Qualcomm Incorporated (QCOM), the chipmaker powering modern connectivity. The company just bumped its quarterly dividend to $0.92 per share, up 3.4% from its prior $0.89, payable in June. It’s not a massive jump, but it does reflect management’s confidence.

Qualcomm rose to prominence by enabling the tech inside everyday connected devices, riding the artificial intelligence (AI) and 5G wave. But the stock has slid 19.62% in 2026, pressured by weak smartphone demand amid a global memory glut and a weak near-term outlook.

While its valuations are cooling and dividends inching higher, is this a wise buy-the-dip moment for investors, or does QCOM have more room to fall?

About Qualcomm Stock

San Diego, California-based Qualcomm is a fabless semiconductor company that powers much of the connected world. It runs through its Qualcomm CDMA Technologies (QCT), Qualcomm Technology Licensing (QTL), and Qualcomm Strategic Initiatives (QSI) segments, blending chip innovation with tech licensing and strategic investments. Currently, its market cap stands at $145.3 billion.

Best known for its Snapdragon processors and 5G modems, QCOM sits inside everything from smartphones to smart homes and even connected cars. After four decades in the game, the company is now pushing deeper into AI-driven computing, energy-efficient performance, and advanced wireless tech. With platforms like Dragonwing, it is also expanding beyond consumer devices into enterprise and industrial markets, aiming to stay relevant as computing spreads everywhere.

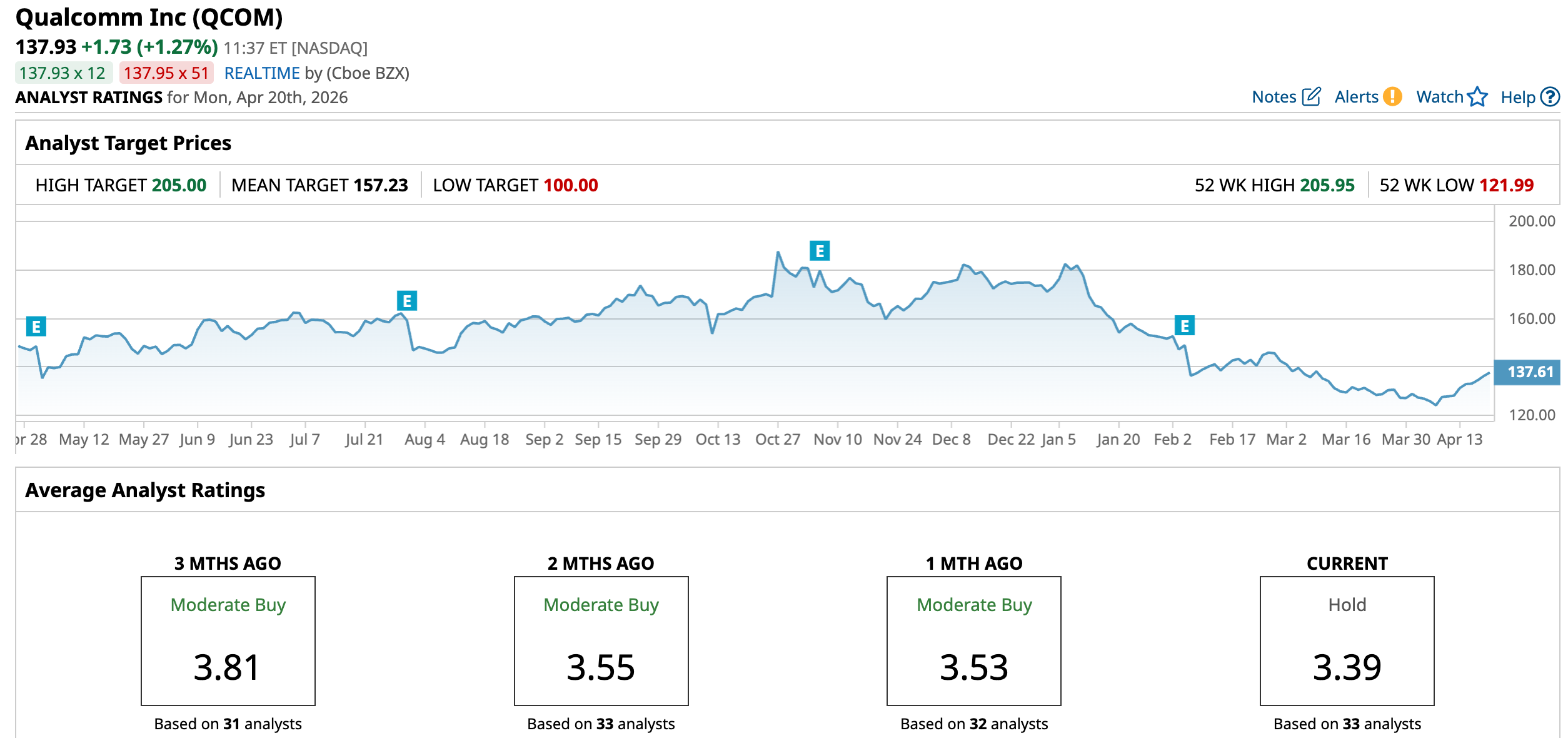

QCOM stock has had a pretty rough run this year. The stock is sitting nearly 33% below its 52-week high of $205.95 from last October. Over the past year, it has not done much, but the real damage has come more recently – down about 10.76% in the last three months and 19.62% year-to-date (YTD).

Back in early January, QCOM was comfortably trading above $180. Now it has slipped below $140, basically erasing a big chunk of the gains it built over the past couple of years and drifting back toward levels seen around 2020. A softer-than-expected outlook in its last earnings report did not help either. It raised fresh concerns about how much growth Qualcomm can squeeze out beyond the smartphone market, which still drives a big part of its business. Investors have seen this story before, and patience seems to be wearing thin. On top of that, a more cautious tone from analysts had added to the pressure.

Yet, it is not all one-way traffic. Some technical signals suggest things might be calming down a bit. The 14-day RSI, which was in oversold territory in February, has bounced back to 63.30 - hinting that the heavy selling could be easing. At the same time, the MACD oscillator has turned positive, with momentum starting to lean slightly bullish. It’s early, but there are signs the slide may be losing steam.

After the recent slide, QCOM stock is starting to look a lot more reasonably priced. It’s now trading at 12.29 times forward adjusted earnings, cheaper than the sector peers and even below its own five-year average. That shift alone is catching the eye of value-focused investors.

And if investors like getting paid while they wait, Qualcomm has been pretty consistent. It has raised its dividend for 22 consecutive years. The latest 3.4% raise takes it to $0.92 a quarter, or $3.68 per share on an annualized basis, with a 2.65% forward yield. Plus, the company’s forward payout ratio is about 29%, so there is still room to keep those hikes coming.

QCOM Slips After Its Q1 Report

Qualcomm began the year on a steady note. On Feb. 4, after the market closed, the company reported first-quarter fiscal 2026 results, with revenue of $12.3 billion, up 5% year-over-year (YOY), and adjusted EPS of $3.50, rising 3% annually. Both the figures came in slightly ahead of consensus expectations.

Performance across segments remained balanced. The high-margin QTL licensing business generated $1.6 billion, supported by improved volumes and a favorable mix. Meanwhile, the core QCT chip segment contributed $10.6 billion. Handset revenue reached a record $7.8 billion, driven by premium smartphone launches. IoT revenue increased 9% annually to $1.7 billion, while automotive rose 15% YOY to $1.1 billion, reflecting continued adoption of Snapdragon Digital Chassis platforms.

Additionally, Qualcomm maintained strong capital returns, distributing $3.6 billion through dividends and share repurchases. The company ended the quarter with $7.2 billion in cash and generated $5 billion in operating cash flow.

But here’s where the mood shifted. The Q2 outlook was soft. Management guided revenue to between $10.2 billion and $11 billion, and adjusted EPS is estimated to be between $2.45 and $2.65 – both below what the Street wanted. The cautious guidance led to an 8.5% decline in the stock in the following session.

Near-term challenges persist, particularly in the global memory market, where AI-driven data center demand is tightening supply and increasing costs for smartphones. Additionally, Chinese device manufacturers are moderating production and inventory levels. While management remains confident in underlying handset demand, near-term softness is expected, with Q2 QCT handset revenue projected at around $6 billion.

The company is all set to release its Q2 results on Wednesday, April 29, after market close.

Analysts currently predict Qualcomm’s Q2 EPS to decline 19.6% YOY to $1.89. Looking ahead, EPS is projected to slip 18.1% YOY to $8.25 in fiscal 2026, but then rise marginally to $8.26 in fiscal 2027.

What Do Analysts Expect for QCOM Stock?

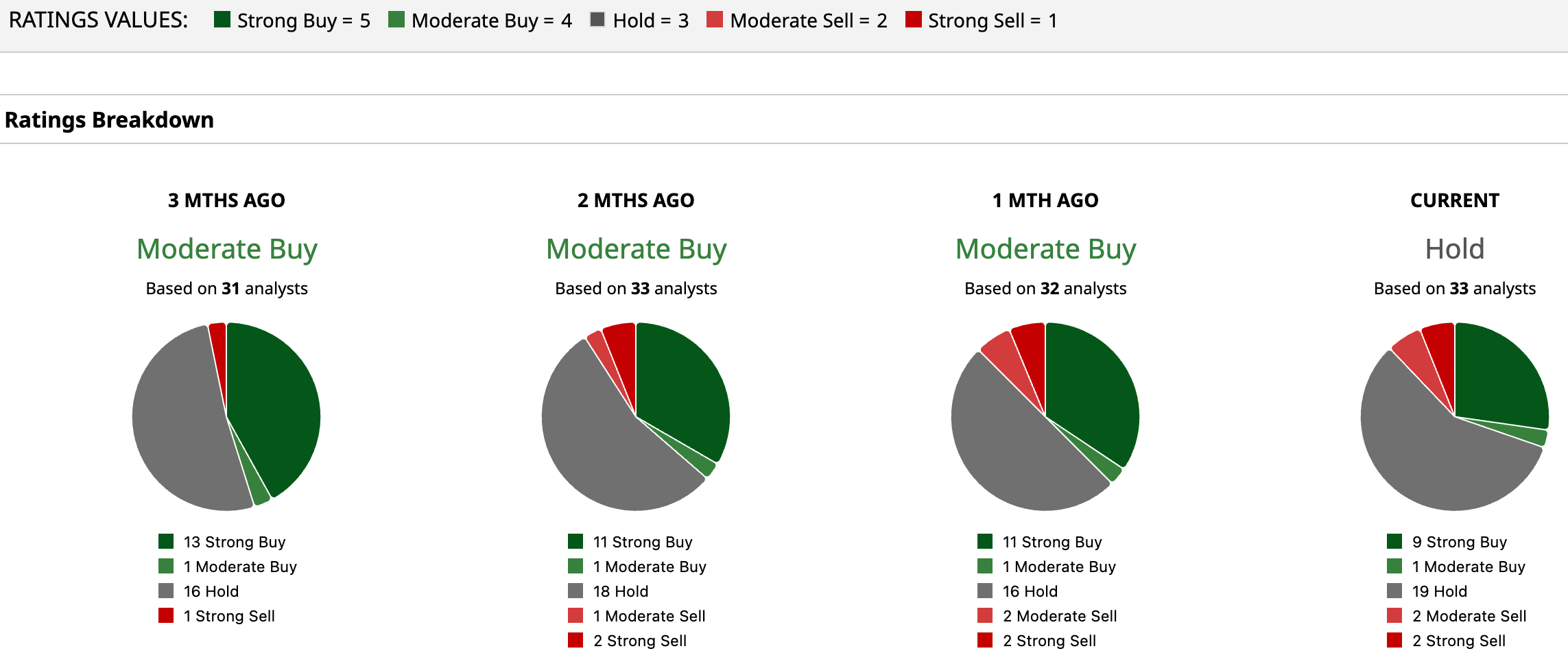

After Qualcomm’s Q1 report, multiple brokerages have expressed caution on QCOM stock. And now, before its Q2 report, JPMorgan is turning a bit cautious on the company, downgrading QCOM stock to “Neutral” and trimming its target to $140. The concern is the ongoing pressure in the handset business, from memory constraints to weak China demand and heavy reliance on a few key customers, while newer growth segments are still not big enough to fully offset the drag.

Overall, Wall Street rates QCOM stock a “Hold,” a downgrade from a “Moderate Buy” a month back. Out of the 33 analysts that cover the stock, nine suggest a “Strong Buy,” one recommends a “Moderate Buy,” 19 analysts are playing it safe with a “Hold” rating, two have a “Moderate Sell,” and the remaining two rate it a “Strong Sell.”

Based on its mean target price of $157.23, QCOM stock has upside potential of 14% from current levels. Its Street-high target price of $205 implies the stock could rally as much as 48.6% in the next 12 months.

Final Thoughts on QCOM Stock

Right now, Qualcomm sits in that in-between zone – it is not broken, but it is definitely not cruising either. The stock has taken a noticeable hit, and near-term growth still looks a bit shaky, especially with pressure on its core handset business. But the bigger picture has not really fallen apart.

The company is still generating solid cash, still profitable, and still expanding into areas like automotive, IoT, robotics, and data centers. Those pieces are not fully showing up in earnings yet, but they are clearly being built out.

The recent dividend hike adds a bit of comfort, showing the company is not stressed on cash and is willing to keep rewarding shareholders. Still, this isn't a no-brainer buy. If one is expecting a quick rebound, the stock might test patience, and the current volatility might not be your friend.

However, for long-term, value-oriented investors who can handle some bumps along the way, the recent dip may start to look appealing. For others, it may be wiser to stay on the sidelines until there is clearer stability and momentum.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Qualcomm Just Increased Its Dividend. Should You Buy QCOM Stock Here?

- As NetApp Expands Its Relationship With Google Cloud, Should You Buy, Sell, or Hold NTAP Stock?

- Dear Seagate Technology Stock Fans, Mark Your Calendars for April 28

- Profit Jumped 58% at Taiwan Semi. Does That Make TSM Stock a Buy Here?